Introduction

Investing in higher education is one of the most significant investments you can make in your future. However, the cost of tuition and other expenses can often be a barrier for many students. That’s where low-interest student loans come in. In this comprehensive guide, we’ll explore how low-interest student loans can help you finance your education and pave the way for a brighter future.

Understanding Low-Interest Student Loans

What Are Low-Interest Student Loans?

Low-interest student loans are loans specifically designed for students that come with lower interest rates compared to traditional loans. These loans aim to make higher education more affordable by reducing the overall cost of borrowing.

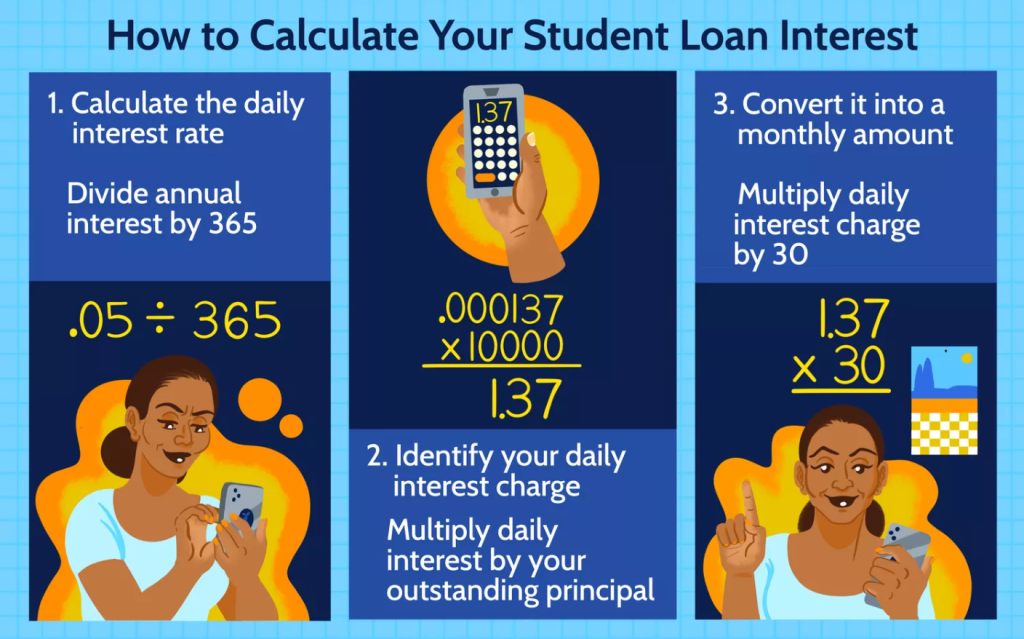

Benefits of Low-Interest Student Loans

The primary benefit of low-interest student loans is their cost-effectiveness. By securing a loan with a lower interest rate, students can save thousands of dollars over the life of the loan, making repayment more manageable and less burdensome.

Qualifying for Low-Interest Student Loans

Eligibility Requirements

To qualify for low-interest student loans, students typically need to meet certain eligibility criteria, such as enrollment in an accredited educational institution, maintaining satisfactory academic progress, and demonstrating financial need.

Application Process

The application process for low-interest student loans may vary depending on the lender and loan program. Students are often required to fill out a Free Application for Federal Student Aid (FAFSA) to determine their eligibility for federal student aid, including low-interest loans.

Exploring Federal Loan Options

Direct Subsidized Loans

Direct Subsidized Loans are federal student loans available to undergraduate students with demonstrated financial need. The government pays the interest on these loans while the student is in school, during the grace period, and during deferment periods.

Direct Unsubsidized Loans

Direct Unsubsidized Loans are available to undergraduate and graduate students regardless of financial need. Unlike subsidized loans, students are responsible for paying the interest on these loans throughout the life of the loan.

Evaluating Private Loan Options

Private Student Loans

In addition to federal loans, students may also consider private student loans offered by banks, credit unions, and other financial institutions. Private loans may have variable or fixed interest rates and repayment terms that differ from federal loans.

Comparing Interest Rates and Terms

When evaluating private loan options, it’s essential to compare interest rates, fees, repayment terms, and borrower protections offered by different lenders. Look for loans with competitive interest rates and favorable terms.

Managing Student Loan Debt

Budgeting for Repayment

Create a budget that accounts for your student loan payments and other financial obligations. Prioritize making on-time payments to avoid default and protect your credit score.

Exploring Repayment Options

Federal student loans offer various repayment plans, including income-driven repayment options that adjust your monthly payment based on your income. Private lenders may also offer flexible repayment plans, so be sure to explore all available options.

Conclusion

Low-interest student loans offer a valuable opportunity for students to invest in their future without incurring excessive debt. By understanding the benefits of low-interest loans, qualifying for federal aid, exploring private loan options, and managing repayment effectively, students can finance their education responsibly and embark on a path toward success.